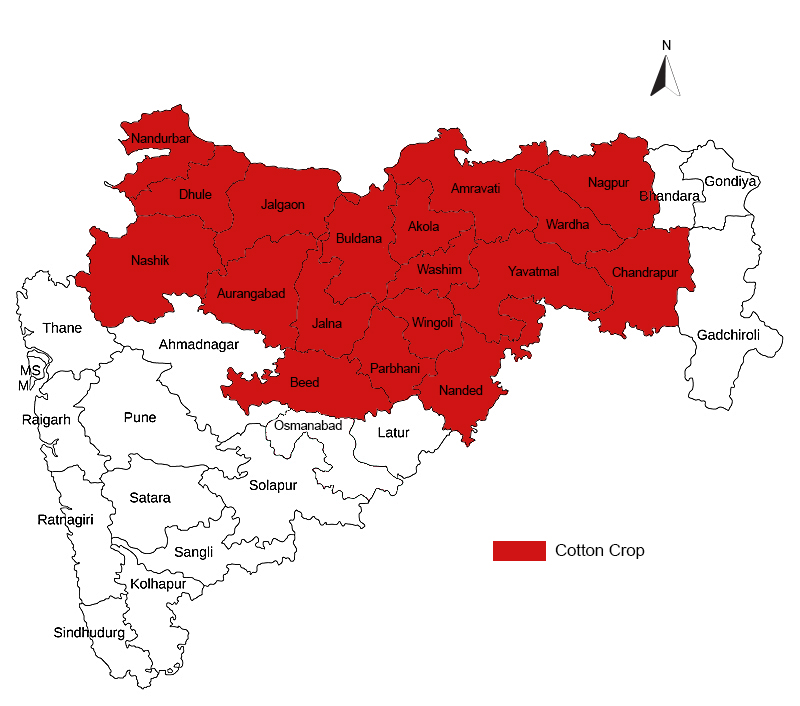

Maharashtra is the largest cotton growing State in the country. It covers about 34% of total cotton area and contributes 17% of the production. Maharashtra produces approximately 25 lakh bales per year.

Factors influencing low productivity

The factors which cause low productivity of cotton in India and particularly Vidarbha and marathwada are as follows:

- Cotton is largely rain fed with uneven distribution of rainfall.

- Bt cotton which occupies most of the cotton area in India and Vidarbha and marathwada requires adequate availability of inputs like water, fertilizers and pesticides to harness its potential of high yield.

- Cotton is also grown in shallow (less than 40 cm in depth) in Vidarbha which is not conducive for high yield.

- Transfer of technology to achieve high yield is not adequate.

- Limited access to institutional finance for the farmers.

- The farmers agree to sell the produce to the buyer and the buyer, in turn, is committed to purchase it at the prevalent market rate.

Details about Pradhan Mantri Fasal Bima Yojana (PMFBY)

To provide financial support to farmers suffering crop loss/damage arising out of unforeseen events, a new scheme namely, Pradhan Mantri Fasal Bima Yojana (PMFBY) has been approved for implementation in all States and Union Territories from Kharif 2017 season in place of National Agricultural Insurance Scheme (NAIS) and Modified National Agricultural Insurance Scheme (MNAIS).

PMFBY is a marked improvement over the earlier schemes on several counts and comprehensive risk coverage from pre-sowing to post-harvest losses has been provided under it. A budget provision of Rs.5501.15 crore has been made for the scheme during 2016-17.

The PMFBY is compulsory for loanee farmers availing crop loans for notified crops in notified areas and voluntary for non-loanee farmers.

Scale of Finance declared by the District Level Technical Committee has been taken as Sum Insured of the crops under the Scheme. There is no capping in premium, however, premium payable by farmers has been substantially reduced and simplified and there is one premium rate on pan-India basis for farmers which would be maximum 1.5%, 2% and 5% for all Rabi, Kharif and annual horticultural/commercial crops, respectively.

Salient Features of PMFBY

- Provide comprehensive insurance coverage against crop loss on account of non-preventable natural risks, thus helping in stabilizing the income of the farmers and encourage them for adoption of innovative practices.

- Increase the risk coverage of Crop cycle – pre-sowing to post-harvest losses.

- Area approach for settlement of claims for widespread damage. Notified Insurance unit has been reduced to Village/Village Panchayat for major crops

- Uniform maximum premium of only 2%, 1.5% and 5% to be paid by farmers for all Kharif crops, Rabi Crops and Commercial/ horticultural crops respectively.

- The difference between premium and the rate of Insurance charges payable by farmers shall be provided as subsidy and shared equally by the Centre and State.

- Uniform seasonality discipline & Sum Insured for both loanee & non-loanee farmers

- Removal of the provision of capping on premium and reduction of sum insured to facilitate farmers to get claim against full sum insured without any reduction.

- viii) Inundation has been incorporated as a localized calamity in addition to hailstorm and landslide for individual farm level assessment.

- Provision of individual farm level assessment for Post harvest losses against the cyclonic & unseasonal rains for the crops kept in the field for drying upto a period of 14 days, throughout the country.

- Provision of claims upto 25% of sum insured for prevented sowing.

- “On-Account payment” upto 25% of sum insured for mid season adversity, if the crop damage is reported more than 50% in the insurance unit. Remaining claims based on Crop Cutting Experiments (CCEs) data.

- For more effective implementation, a cluster approach will be adopted under which a group of districts with variable risk profile will be allotted to an insurance company through bidding for a longer duration upto 3 years.

- Use of Remote Sensing Technology, Smartphones & Drones for quick estimation of crop losses to ensure early settlement of claims.

- Crop Insurance Portal has been launched. This will be used extensively for ensuring better administration, co-ordination, transparency and dissemination of information.

- Focused attention on increasing awareness about the schemes among all stakeholders and appropriate provisioning of resources for the same.

- The claim amount will be credited electronically to the individual farmer’s Bank Account.

- Adequate publicity all the villages of the notified districts/ areas

- Premium rates under Weather Based Crop Insurance Scheme (WBCIS) have also been reduced and brought at par with new scheme. Further, capping on Actuarial premium and reduction in sum insured has been removed in this scheme also.

- In addition, a Unified Package Insurance Scheme (UPIS) has also been approved for implementation on pilot basis in 45 districts of the country from Kharif 2016 season to cover the other assets/activities like machinery, life, accident, house and student-safety for farmers along- with their notified crops (under PMFBY/ Weather Based Crop Insurance Scheme – WBCIS).

Farmer’s reaction on crop insurance for cotton crop

The cotton crop which is highly grown over area in the region of marathwada and vidarbha of maharashtra state. The crop included in the Pradhan Mantri Fasal Bima Yojana (PMFBY) in kharif season.

We were discussed with farmers who grown the cotton crop about crop insurance scheme and we found the government is collecting five percent premium per hector from the cotton crop growers, being as an cash crop premium is higher than other kharif and rabbi crop.

By receiving past three year it is found the losses to the farmers due to cotton growing were negligible that’s why farmers not getting the insurance money that’s why farmer now giving priority to the others crop for the crop insurance.

in some area it is found that cotton crop was infested with the cotton bollworm but losses were also negligible.

According to government scheme the farmers who takes the loan has to pay premium compulsory by highlighting the points mainly all farmers takes the loan.

Nowadays due to development of highly quality varieties such as BT cotton as genetic modified crop, these varieties are less susceptible to the disease and pest so losses are lower to the farmer or we can say negligible.

We were also discussed with agriculture officer after discussion with all they were talking that in past three to four years except draught condition, no losses were found to give the insurance money to the cotton growers.

Farmers were taking that they were not getting rate to crop according to cultivation cost.

Conclusions

- As a cash crop, cotton crop having highest five percent and farmers want to cut this premium to lowest.

- No losses observed, in cotton crop that’s why farmers not getting benefits of crop insurance scheme.

- Some farmers not having knowledge about Pradhan Mantri Fasal Bima Yojana (PMFBY).

Good Information